It is the ability of a company to meet its payment obligations in a generic way or in the medium-long term.

The solvency ratio can be defined in an aggregate way as the quotient between total assets and liabilities. Ideally, the value of this ratio should be greater than 1.5, but it is interesting to analyse the composition of assets and liabilities. However, it should be noted that the value of this ratio would depend on the sector or type of business in question. Therefore, in addition to observing that the ratio is greater than 1.5, it is advisable to see its evolution over time.

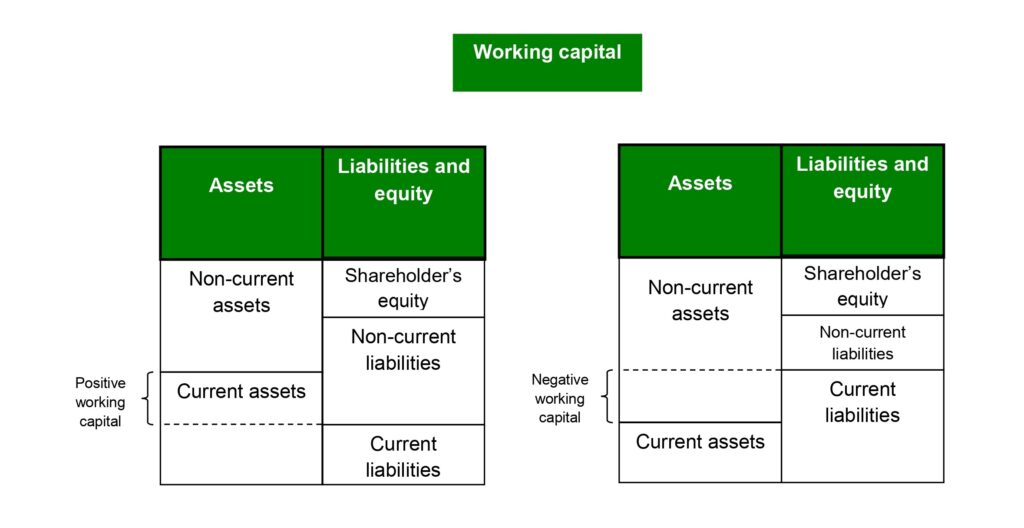

A very important concept when assessing the solvency situation of a company is the so-called working capital.

Working capital can be calculated by subtracting non-current assets from the sum of equity and non-current liabilities, or by subtracting current liabilities from current assets:

- A positive working capital means that the company’s own funds plus non-current (long-term) liabilities not only cover the non-current assets, but there is a remainder that supports part of the current assets. A positive working capital is a sign that the company has a good short-term financial position.

- A negative working capital is produced when current liabilities exceed current assets, with which the company will find itself with short-term debt maturities that it will not be able to meet with the realization of current assets. However, it should be noted, as in the case of the solvency ratio, that certain companies could operate with a negative working capital.

The following diagram represents the above: