Over time, the agents that make up an economy (companies, families, governments, etc.) must take a series of decisions regarding different aspects related to production, consumption, savings and investment.

Such decisions are very important for each agent individually, but, when aggregated, they are also very important for society as a whole. Economic agents must not only decide what type of decision to take, but also to what extent.

At some point in time, some agents will want to carry out spending projects and may not have the necessary resources to deal with them. On the contrary, other agents, who decide to postpone their spending projects for the future, may have resources available that they will not need to use at present.

Because of the foregoing, economic agents will find themselves in one of these two situations:

- Deficit, or in need of financing (the available funds are less than the necessary funds).

- Surplus, or with financing capacity (the available funds exceed the necessary funds).

Therefore, in the absence of financial activity, the economic agents that were in a deficit situation would see their possibilities of choice reduced, while those that were in a surplus situation would maintain idle resources. In both contexts, the well-being of economic agents would be below the optimal and desired level, and the same would happen to the well-being of society as a whole.

Given the situation described, agents with financing capacity may be interested in transferring their savings for a certain period to those who have a deficit position.

However, this process is unlikely to take place directly for a number of reasons:

- It is difficult for the amounts of the resources to coincide for both parties, as well as the period required by each one.

- The saver may not currently need to use their money, but may wish to do so when they see fit.

- In addition, the person who has resources available may not be willing to take the risk of handing them over to just anyone.

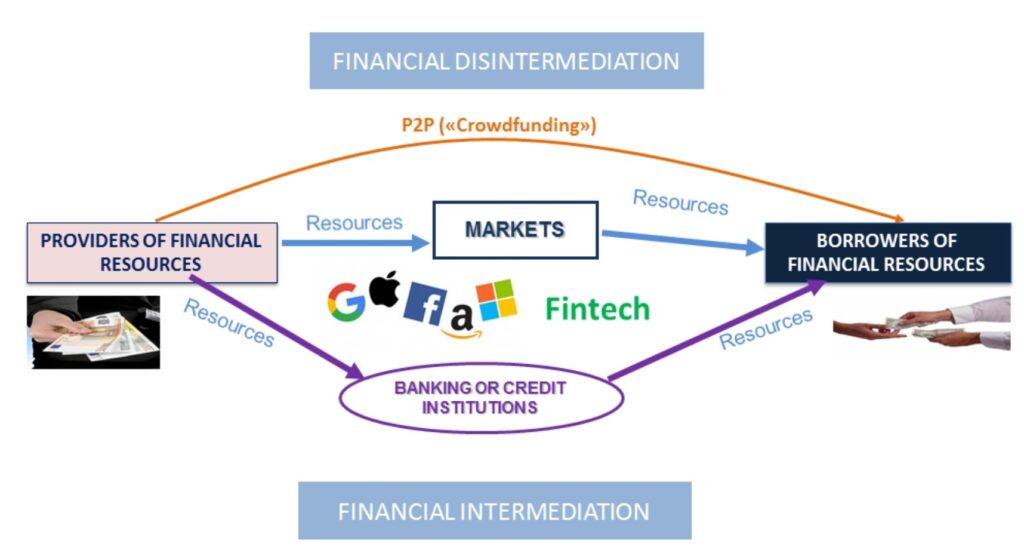

For all these reasons, it is not possible to expect that the different economic agents will easily reach agreements in savings and loan transactions, which are essential for the functioning of any economy. To fulfil this role of connecting agents with financing capacity with those in need of financing, every country has a financial system.

The financial system puts savers in contact with investors and makes it possible to reconcile the preferences and needs of both groups in terms of amount, term, return and risk.

Considering the above, the financial system of an economy can be defined as the set of institutions, means and markets whose primary purpose is to channel the savings generated by economic agents with financing capacity to those others who, at a given time, are in need of financing, a process illustrated below: