There are different types of loans, which can be classified according to different criteria, which can be combined with each other:

- To individuals or legal entities.

- For consumption or for productive activities.

- For housing or for other purposes.

- At fixed interest or variable interest.

- Short term or long term.

- With a personal guarantee or secured.

From this classification, the most relevant distinctions will be described below, based on the collateral of the transaction for the benefit of the lender. Considering the collateral, the following types of loans can be distinguished:

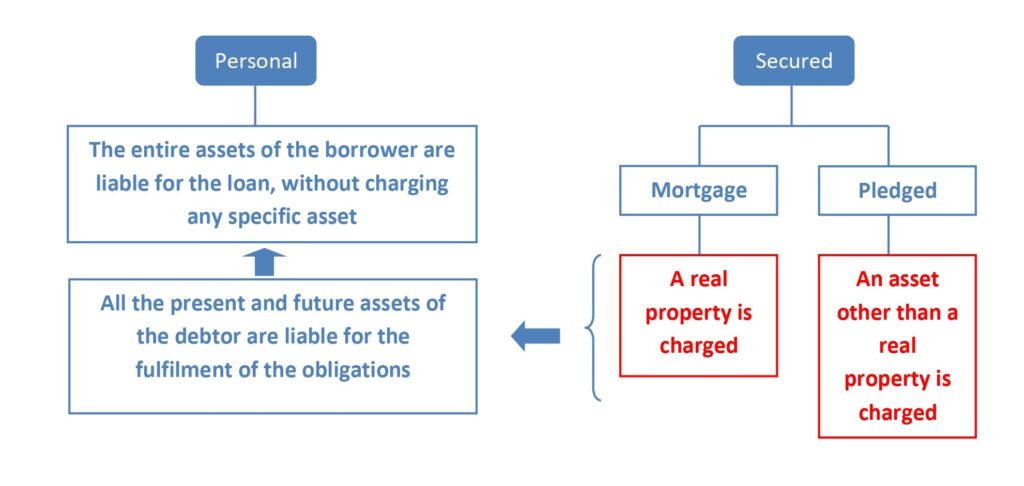

- Personal guaranteed loans: The whole of the present and future assets (goods and rights) of the borrower are liable for the loan in a general way, without any specific good being charged or subject to the payment of the loan in a special way. In personal guaranteed loans, if the borrower defaults on their repayment commitment and fails to pay the repayment instalments, the lender may judicially seize assets or rights owned by the borrower.

- Secured loans: In this type of loans, a specific asset or right is subject to the payment of the loan, in the event that the borrower cannot meet the obligations undertaken. This security interest, in turn, can be of a double nature: If the asset pledged as collateral is a movable asset, it is a pledge, and if it is a real property, it is a mortgage.

The most important type is that of loans with a mortgage guarantee, in which the guarantee of the loan is a real property, usually acquired with the amount of the loan itself.

- Pledged loans: In this type of loans, the guarantee is constituted on assets other than real estate, such as term deposits, investment funds units, shares, debentures, etc., which will generally be deposited with the same creditor institution.

The following diagram summarizes the differences between a personal loan guarantee and a secured loan:

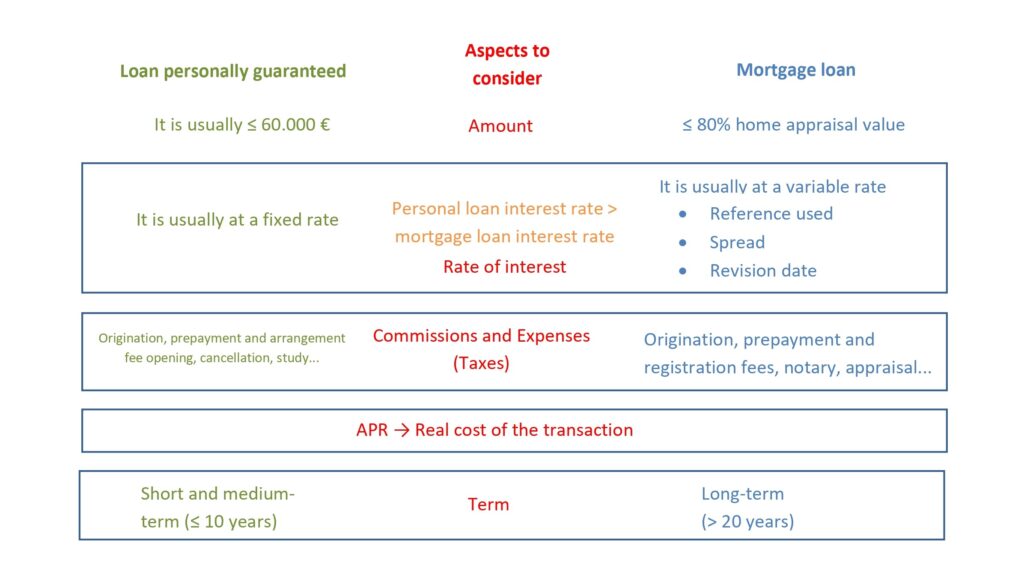

Although there is no fixed rule, personal loans granted to individuals generally have an amount that usually does not exceed a certain limit and their term is usually less than 10 years. If the purpose of the loan is to finance a real property (home, country estate, commercial premises, etc.), the amount must be less than 80% of its appraisal value and they are granted with long-term maturity, which may be higher than 20 years.

In personal loans, as they do not have specific tangible collateral, as occurs in mortgage loans, and therefore they present a higher degree of risk for the lender, the applicable interest rate is usually higher. In these transactions, it is usual that they are agreed at a fixed interest rate. While in mortgage loans, since the property itself is financed as a guarantee of the transaction, the risk taken by the financial institution is mitigated, so the interest rate charged is usually lower. It is usual that a variable percentage rate (reference rate used plus a spread) to be agreed subject to revision on the dates stipulated in the contract.

In both types of loans, it is necessary to take into account the commissions, the different expenses and taxes that occur when launching the transaction, since knowing them will allow us to value the effective cost that a person who takes out a loan transaction has to face (in its relationship with the lender), that is, the annual percentage rate, known by the acronym APR.

In order to facilitate the comparison of the information regarding interest rates offered by the different institutions, the regulations require them to communicate to their customers the APR (annual percentage rate payable at matured term equivalent) which, in accordance with the applicable interest rates, terms, commissions and other contractual conditions, results in each case, according to the mathematical formula established for this purpose.

The following diagram shows the main differences between a personal consumer loan and a mortgage loan, which have been explained above: