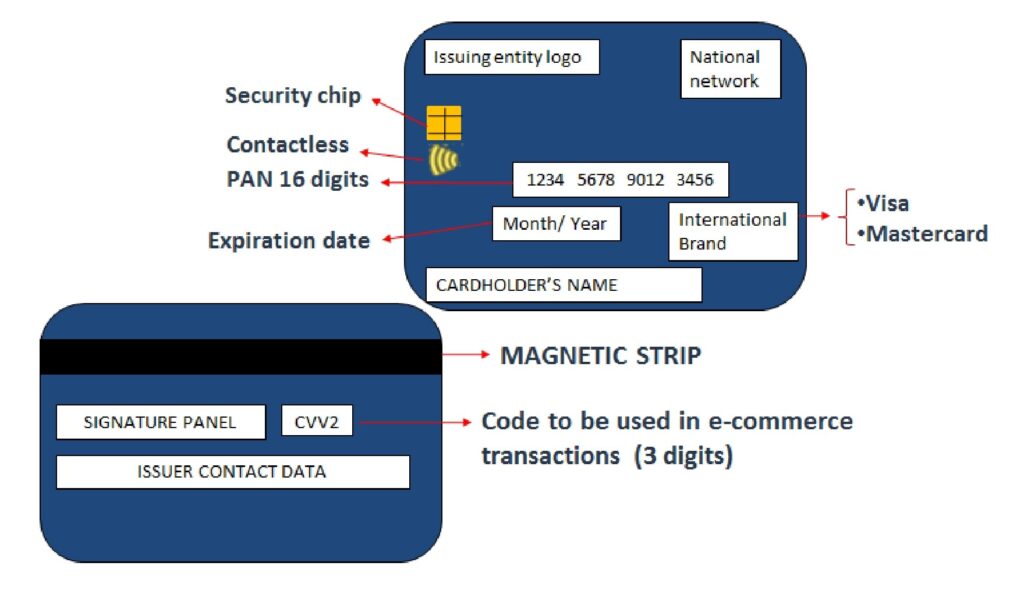

Among the means of payment, cards stand out, being a payment instrument whose support is a plastic (even a cellular phone in which the card is “uploaded”) and which allows you to pay instantly, as if you were carrying physical money, to withdraw money at ATMs and even to finance the purchase of goods and services. The following diagram shows the fields of a card:

The economic transactions carried out with a card are possible thanks to the data entered via magnetic stripe (dark band that is incorporated into the card in which information is encoded in order to be able to operate with it) or chip (small integrated circuit that performs numerous functions in computers and electronic devices).

In payments made remotely over the Internet, the cardholder is usually asked to provide the PAN (numbering of the card that appears on its front), the expiration date, and the security code designed specifically for this operation (CVV code) that is reflected on the back of the card.

There are different types of cards, such as, for example, debit cards that allow you to operate through ATMs (to withdraw money, to request statements and account movements, etc.), as well as to pay in stores and shops. In this type of card, every debit item for the transactions carried out is immediately deducted from the customer’s account balance; if there is not enough balance, the transaction cannot be carried out. However, there are exceptions, such as the case of so-called off-line transaction: When there is no immediate connection with the financial institution, the transaction is carried out without checking the balance; an example of this system is the payment of tolls on motorways.

Another type of cards are credit cards, which are cards that have an associated credit facility, so it can be decided that the amount drawn is debited directly to the associated or linked account (in the manner of a debit card) or that the payment is made from the credit facility, being able to choose different ways to repay the drawn-down amount, such as the payment at the end of the month, or a fraction thereof (fixed monthly instalment or percentage of the total amount spent). A credit limit is established for each card. In addition, credit cards allow you to carry out in a general way the following transactions: Purchases (in stores or online) and cash withdrawals at ATMs.

Currently, most financial institutions allow their credit and debit cards to be used to carry out other transactions, such as cash transfers to the associated account, cash withdrawals at the counter, payment of taxes and balance transfers to other cards.

Attention must be paid to the interest rate charged for the deferral of payment of the transactions carried out. The deferral of payment implies the collection of interest, which will depend on the time that elapses since the funds are available and the amount of such payment.

Within credit cards, we find the revolving type. This is the name given to those in which all payments are deferred, with the particularity that, in exchange for the payment of a fixed instalment, once the amounts drawn down have been paid, in whole or in part, the balance is available again in the corresponding amount.

We can also find other types of cards, such as the so-called prepaid cards, that limit their use to the amount previously paid into them.

Thus, first the money (previously paid) is loaded into it in order to be able to carry out the transactions that you want.

The advantages it offers are that it allows you to limit payments, since only the amounts previously paid are spent and it allows you to buy on the Internet safely, since only the amount of the transaction previously loaded is risked.

Finally, and to meet the needs of the growing electronic commerce, the so-called virtual cards were created. With them, you can make payments over the Internet or mobile phone, avoiding the presentation of a physical card.

The virtual card offers a higher level of security than traditional cards for purchases made over the Internet or by mobile phone, as they are valid for a single transaction.

Before making the purchase, the customer, through the website of their financial institution or an authorized operator, must request a “virtual card” appropriate to the purchase they want to make.

Finally, the data to be used in the purchase will appear on the computer screen.

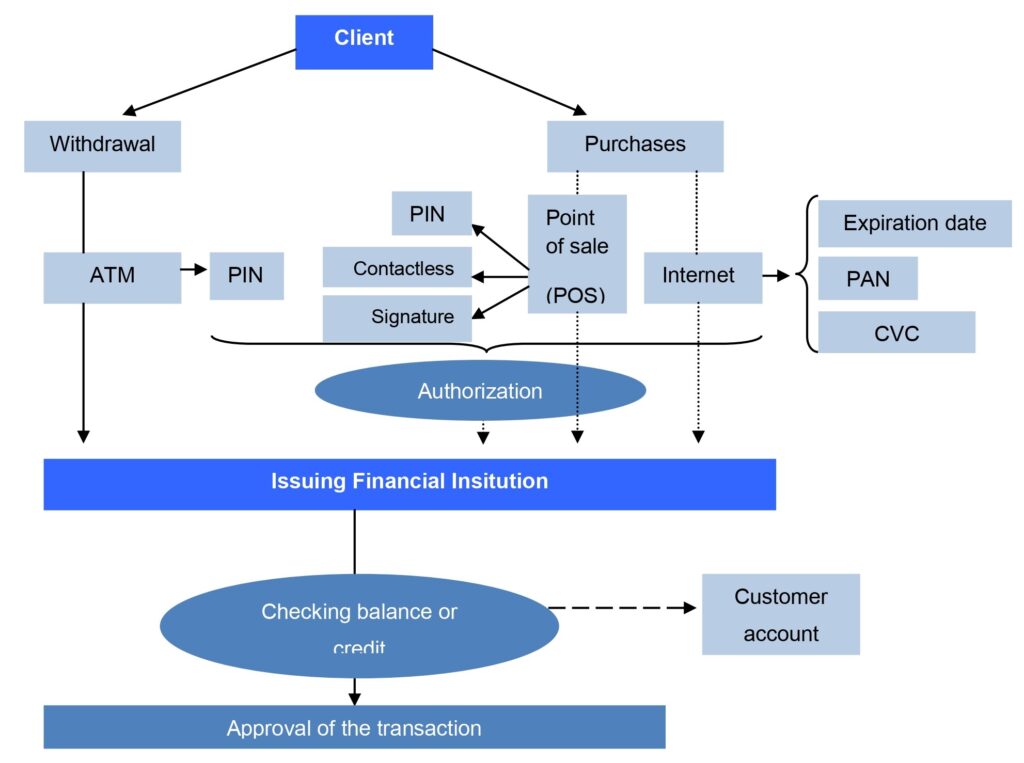

How a card works

With a card, a person can withdraw money (withdrawal) or make a purchase. In the first case, you go to an ATM and you are asked for the card PIN (personal identification number); after authorization, the issuing financial institution is accessed to check the balance or find out if it has a credit facility, accessing the customer account; if correct, the transaction is approved.

In the case of a purchase, it can be done through a POS (point of sale) terminal, requiring the PIN for authorization, or through the Internet, needing to enter the expiration date, the PAN and the CVC of the card as well as a sort of additional authentification; afterwards, the process would be the same as the previous one; the issuing financial institution checks the balance or if it has a credit facility by accessing the customer account, and, if it is correct, the transaction is approved.