Definition

Factoring consists of an administrative-financial service through which the company transfers the collection rights —trade receivables that it has in its portfolio— to a specialized financial institution (the factor), with the purpose of managing, and, optionally, advancing their collection.

In addition to the financial function, that is, mobilizing short-term receivables, factoring offers different management and administration services, as well as the possibility of protecting itself from the risk of non-payment of the trade receivables assigned.

Services that factoring can offer:

- Financing of working capital, through financial advances on assigned invoices pending collection.

- Guarantee in the event of insolvency of the debtors (the assignor’s clients).

- Collection process of assigned invoices.

- Administration and classification of the assignor’s client portfolio.

There are always three parties involved in a factoring relationship:

- The customer, who is called the assignor.

- The clients of the former, called debtors.

- The financial institution, called a factor or factoring company.

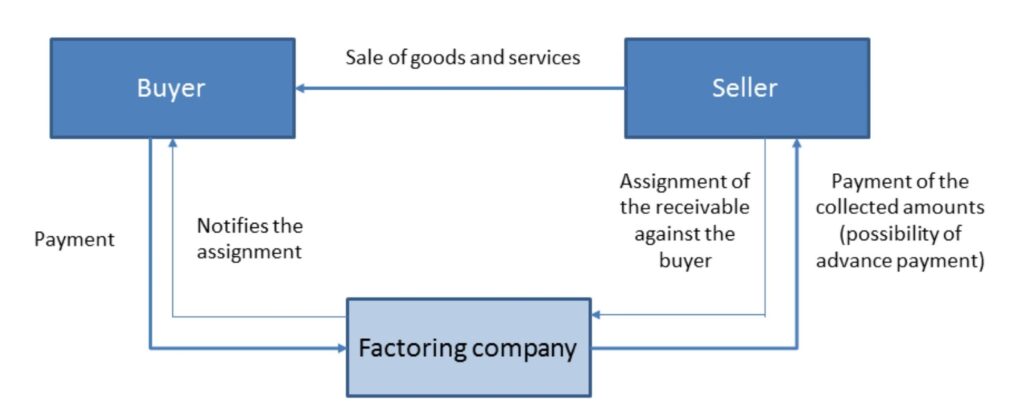

A simple diagram allows you to see the types of relationships that are established between the parties and their operation:

The factor analyses the entire client portfolio of the supplier, determining the total assignment volumes of the portfolio and the percentages and volumes per client. Once these conditions have been established, the supplier informs its clients that, from that moment, they will have to pay such invoices to the factoring company.

Once the contract is concluded, the supplier communicates to the factor the invoices it has issued to each client and the payment conditions established with such client.

Depending on the needs of the supplier, the factor can advance them the collection or wait until the invoices are due to make the payment. Likewise, the factor will inform the supplier of the situation it has with each of its clients.

Upon expiration of the invoice and under the conditions established between the supplier and its client, the factor collects from the latter the amount of the invoices issued by the supplier.

Types of factoring

There are different types of factoring:

1) According to the financing provided:

- Invoice factoring: The client can raise financing based on the assigned invoices.

- Maturity factoring: The client does not have the right to request financing.

2) According to risk coverage:

- Recourse factoring: The factoring company is not liable for the insolvency of debtors.

- Non-recourse factoring: The factoring company takes the risk of insolvency of the debtors, and is liable for it towards the assignor.

3) Other types of factoring

- Export factoring: It is a factoring for sales made abroad, the debtor being a foreign company, and it provides for the same services and procedures as traditional factoring. As a differentiating element, apart from the location or residence of the debtor, the invoice is denominated in a currency other than the euro.

Advantages of factoring

Factoring provides several advantages, such as:

- It allows to increase the liquidity of the balance sheet and to provide resources to finance the growth of sales.

- Financing on invoices, covering the entire collection period: From the issuance of the invoice until its payment.

- Flexible financing: The assignor has the right to get a financing advance, but is not obliged to request it or accept those offered by the factoring company, so it can regulate the amount of financing and control its cost.

Factoring costs

What is the cost of a factoring?

- Cost of signing the contract

- Commitment fee: A percentage calculated on the taken out facility.

- Commitment fee over the extension of a contract facility: A percentage calculated on the difference between the existing facility and the new one, that is, on the extension tranche.

- Notary fee for contract supervision by a Notary Public.

- Cost of invoice management

- Factoring commission: Consists of a percentage calculated on the nominal amount of each assigned invoice. It depends on the amount of the facility and the advancing period.

- Commission for document handling (invoices and / or promissory notes): It is specified in a fixed amount per invoice.

- Cost of financing advances

When so agreed in the contract, the assignor can get financing from their invoices up to the maximum limits or the percentages indicated in the contract. The assignor does not bear any cost by the fact of agreeing by contract the right to get a financing advance from the assigned invoice. Financial costs only accrue when advances are actually extended by the factoring company at the request of the assignor.

Factoring operation

- Administrative simplicity:

- Written contract supervised by a Notary Public, in which the rights and obligations of both parties are established.

- A single notification to the debtors is sufficient for the implementation of the contract.

- To assign the receivable to the factor and receive the services agreed in the contract, a simple assignment clause is enough in each invoice.

- The factoring company periodically sends information on the status of the invoice portfolio, with all the necessary details for its control, customer-to-customer and invoice-to-invoice.

- Collection certainty:

- In the case of non-recourse contracts, the insolvency risk of debtors is taken by the factor. In these contracts, if the debtor stops paying due to an insolvency situation, the factor covers the amount of the invoice by paying the assignor the amount of the agreed compensation.

- In the case of recourse contracts, although the factoring company does not take the insolvency risk coverage, it professionally manages the collection.

General characteristics of factoring

A factoring can be described by the following characteristics:

- Purpose: Receiving funds through the assignment of trade receivables, as well as the provision of administration services and customer collection process.

- Amount: It is usually advanced a percentage of the assigned invoices; its depends on the factoring method. The rest remains as retention amount and is paid at the time of collection from the customer.

- Transferable documents: It is enough that they are invoices or delivery notes duly stamped and signed. In general, any collection document commercially admitted.

- Exclusiveness: Assignment of all billing and relationship with a single factoring company.

- Interest payments, by means of a discount, in case of funding utilization: The number of days for the calculation of interest includes those that go from the date of receipt of the invoice, delivery note or similar document until its expiration date.

- Guarantees: The main guarantee, in the case of financing, is set by the advance documents themselves (depending on whether the transaction is a recourse factoring or a non-recourse factoring).

- Formalization: By a specific contract.

- Term: It is usually one year, at the end of which the contract can be renewed.