An insurance is a contract by virtue of which, in exchange for the payment of a premium, the insurer undertakes to compensate (indemnify) the insured in case they suffer any contingency in their person or property provided for in the policy. It is, therefore, a protection mechanism against possible risks that may occur.

There are multiple types of insurance, differentiated especially according to the object of the coverage. Thus, we find life insurance, accident insurance, health and healthcare insurance, fire insurance, etc. Usually a distinction is made between life insurance (sometimes personal insurance is also mentioned, including in this concept, in addition to life insurance, health and personal accident insurance) and general insurance (or non-life).

Combined savings insurance

Although there may be different types of combined savings insurance, the most common is that this insurance involves the payment of a single premium by the insured in exchange for taking out, through a single policy, two coverages: One of them guarantees the recovery of the total capital invested and the other is the one that provides regular income, operating in practice as follows:

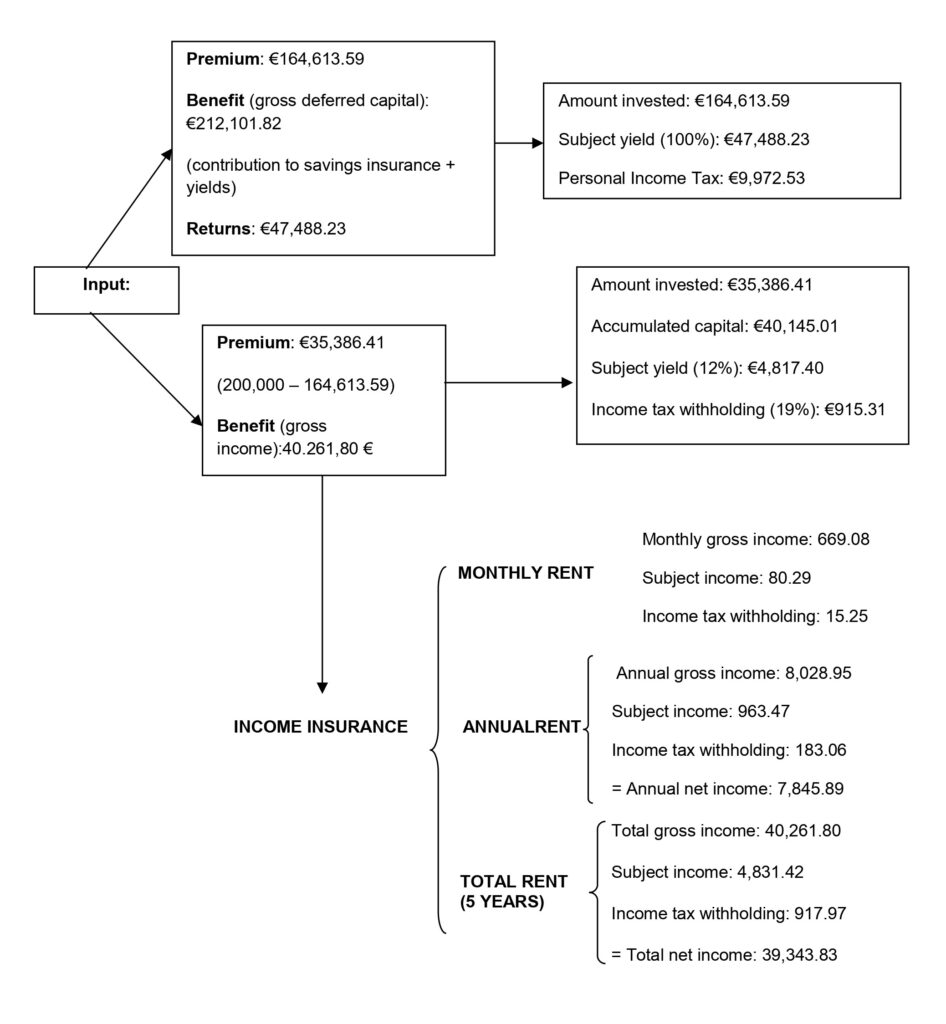

- Deferred capital savings insurance, designed to guarantee the receipt of a certain capital at a predetermined time. The amount necessary to guarantee the receipt of a final capital equal to the initial amount that the client is willing to invest in the product will be allocated to this insurance.

Concepts to keep in mind:

- Premium calculation: The premium is calculated based on the guaranteed interest rate offered by the financial institution and the applicable taxation. In this way, the premium becomes the amount necessary so that, at the end of the term of the contract, the insured receives the total net refund of the contribution made.

- Net deferred capital: It will be the total capital that the insured will receive from the financial institution after the term of the contract, once the corresponding tax has been deducted. Its amount is calculated as the sum of the contribution made to this savings insurance plus the yields received, and subtracting from such amount the tax amount corresponding to the income tax.

- Yields: The yields received will be the difference between the benefit and the premium paid.

- Immediate temporary income savings insurance, the objective of which is to guarantee a certain monthly income. The difference between what the client is willing to invest in the combined savings insurance and what they have already contributed to the deferred capital savings insurance will be allocated to this insurance.

Regarding this insurance, the following aspects should be noted:

- Premium: It is made up of the difference between the client’s total contribution and the amount that they have already invested in the deferred capital insurance (its premium).

- Benefit (gross income): It is the result of applying a guaranteed interest rate to the premium. Normally, the money allocated to income insurance is invested by the financial institution in some products: Fixed income, deposits, etc., and, depending on the products where this amount is going to be invested, it is determined what the nominal rate of the loan transaction will be.

Finally, combined savings insurance usually includes a guarantee in the event of the death of the insured. In these cases, the risk premium comes into play, which, as in any other insurance, will be determined by certain factors of the insured, such as their age. This risk premium represents an additional cost in the combined savings insurance, causing the insurance premium to rise. Additionally, in most cases a health questionnaire is usually completed.

Example: 5-year combined savings insurance for a 52-year-old man, at a guaranteed rate of 5.20%, for the contribution of €200,000 (tax data relating to the 2021 financial year).