The letter of credit, although its name may suggest a credit transaction, is merely a means of payment by which a bank, by order of the importer, irrevocably commits to make the amount agreed on the invoice available to the exporter, conditioning it on true and correct compliance with the conditions set out in the wording of the credit. It is similar to the figure of the guarantee, implying a collection guarantee for the exporter that complies in a timely manner with the conditions included in the letter of credit. The importer, on their part, has the certainty, through the documents received, that they will receive the merchandise in the agreed term and manner.

The issuing institution pays against presentation of the documents, not being liable for the quality, quantity and condition of the merchandise, being transactions independent of the contracts signed by the parties. Therefore, it is a risky transaction that must be previously analysed and approved by the institution that issues the letter of credit.

Types of letters of credit:

In practice, it can be classified as:

- Irrevocable: No credit term can be modified without the agreement of all parties. Today, all the letters of credit issued are irrevocable.

- Confirmed: The issuing bank of a letter of credit is located in a country other than that of the exporter and beneficiary of the credit. The exporter, seeking maximum collection guarantees, can demand confirmation of the credit by a financial institution other than the one that issues it, appearing the role of the reverse factoring bank that adds its irrevocable commitment to the beneficiary, under the same conditions as the issuing bank, guaranteeing that it will collect the amount of the credit if it complies with its terms and conditions. Normally, the reverse factoring bank usually acts also as advising bank of the exporter’s credit.

- Transferable: When a letter of credit is expressly opened as “transferable”, the exporter is being given the possibility of transferring it in whole or in part in favour of one or more beneficiaries. It is typical of transactions managed by intermediaries.

- Sight or time: Depending on whether the payment must be ordered at the same time that the documents be presented or after the deferral period agreed between the parties.

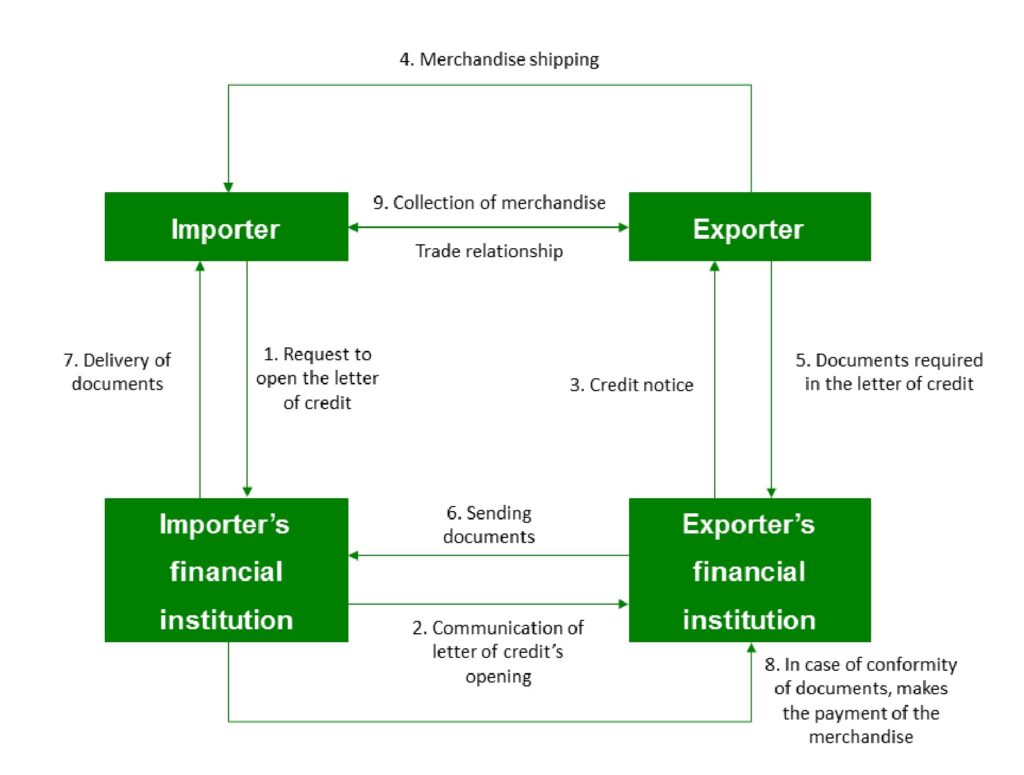

The circuit of a letter of credit can be outlined as follows:

1. The importer asks their financial institution to open a letter of credit in favour of the exporter, indicating the purpose of the credit and the conditions of the transaction, as well as the documents that the exporter must send to prove compliance with their part of the contract and the shipment of the purchased merchandise. The issuance of an import letter of credit supposes a risky transaction that must be previously analysed and assessed by the importer’s institution.

2. The importer’s financial institution issues the letter of credit.

3. Notice of letter of credit to the exporter.

4. The exporter ships the merchandise to the importer in the agreed terms.

5. After shipping the merchandise, the exporter delivers the documentation required in the credit conditions to its financial institution.

6. The exporter’s bank will send the documentation to the issuing institution of the letter of credit.

7. If the documentation received is correct, the importer’s financial institution will order the payment of the agreed amounts to the exporter and will deliver the documents to the importer.

8. The importer removes the merchandise shipped by the exporter at the agreed place.