The pension plan is the instrument that regulates the savings formula that seeks to provide participants with capital, income or a combination of both, which will be the result of the contributions made throughout working years, plus the return derived from their investment.

There is a wide range of types of pension plans that allow the saving effort to be adapted to each stage of working years. When the time comes, you can choose the type of benefit that best suits the recipient’s family and financial situation.

These are the parties involved in a pension plan:

- Promoter: Any entity, corporation, society, company, business association, union or group of any kind that encourages its creation or takes part in its development has such consideration. When it comes to:

- a company, for its employees: It will be an occupational pension plan.

- an association, for its members: It will be an associated pension plan.

- a financial institution, for its clients: It will be an individual pension plan.

- Occupational and associated pension plans have very specific characteristics and do not depend only on the private initiative of the saver, as is the case with individual pension plans.

- Participants: They are the natural persons for whom the plan has been established:

- in the occupational type, they will be the employees.

- in the associated type, the members of the association or group.

- in the individual type, the clients of the financial institutions that take out the plan.

- Beneficiaries: They are the people with the right to receive benefits from the plan:

- the participant himself, in the event of retirement.

- other designated persons, in the event of the participant’s death.

In addition, it will be necessary:

- A management company that manages and invests the assets of the pension fund. They are public limited companies with an exclusive corporate purpose and require express authorization from the relevant body, and to be duly registered in the special administrative registry of that body; and

- A custodian that is in charge of the safekeeping and deposit of the fund’s assets. They are credit institutions domiciled in the country that need to have express authorization from the relevant body, and to be duly registered in the special administrative registry of that body.

We can find several types of pension plans:

- Depending on the type of investment:

- Short-term debt.

- Long-term debt.

- Mixed debt.

- Mixed equity.

- Equity.

- From the point of view of the promoter and the participants:

- Individual pension plan: The one promoted by a financial institution to market it among its clients, these being the only ones who can contribute to the plan as participants.

- Associated pension plan: The promoter of the same will be any association or union, and the participants their associates or members. Contributions are made exclusively by participants.

- Occupational pension plan: The promoter of the same is the entity or individual businessperson that acts as employer of the participant. Thus, any employee of the promoter may acquire the status of participant. The contributions are made by the company on behalf of the participant-employee. If the regulation of the plan contemplates it, the participant-employee can also make supplementary contributions to the occupational plan.

The contributions made to the plans can be of two types:

- Regular: Usually on a monthly, quarterly, semi-annual or annual basis. Automatic annual increases can be agreed-upon through a pre-established fixed percentage, through an additional fixed amount, depending on the increase in the CPI, etc.

- Extraordinary: Those carried out by the participant without an established frequency. They are compatible with regular contributions.

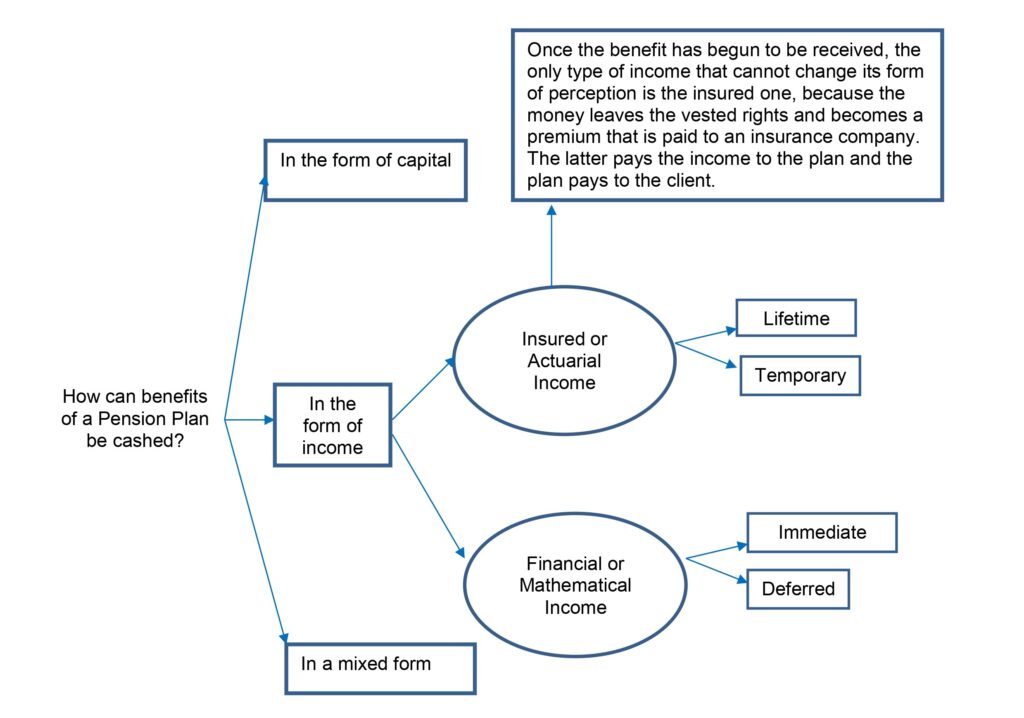

Upon retirement or any of the special contingencies that give the right to receive the amount accumulated in the pension plan, we can cash it in three ways:

- In the form of capital: The totality of the accumulated rights is received all at once (in a single payment).

- In the form of income: It consists of a regular income according to the way in which the beneficiary decides (temporary, lifetime…). A total settlement of the balance pending collection can be made at any time.

- In a mixed form: A part in the form of capital and another in the form of income.