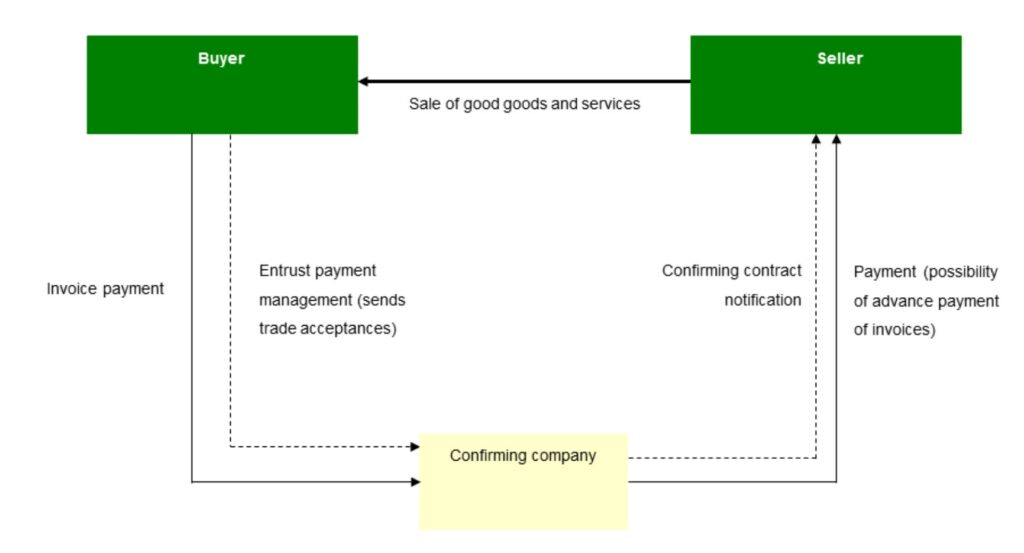

Definition

It is a financial-administrative service that is offered to companies to delegate the administrative management of payment to their suppliers, who, additionally, can advance the collection of their invoices. On the other hand, the companies pay the invoices on the due date agreed with the supplier, having the option of financing them through a credit agreement, in which the payments will be charged to the suppliers. Reverse factoring admits payment to foreign suppliers.

In short, there are two (or even three) products in one:

- Administrative management of payments to company’s suppliers (reverse factoring company), combined with the possibility of getting funding through a credit agreement.

- Possibility of financing the company’s suppliers:

- In a way, reverse factoring is the other side of factoring, but with the addition that the financial institution can formalize asset-side transactions both with the client company (reverse factoring company) and with its suppliers. When the supplier agrees to accept the offer of advance payment of the invoices sent by the institution, it will assign the trade receivables in its favour, as in recourse factoring.

- The banking institution analyses the financial solvency of the reverse factoring company, which is the one that must pay the invoices when due and, therefore, concentrates the risk of the transaction.

General characteristics of reverse factoring

A reverse factoring can be described by the following characteristics:

- Purpose: Administrative management of payments to suppliers of the company and offering of advance payment of invoices to them, as well as financing to the reverse factoring company.

- Amount: The financial institution may limit the amounts, according to the risk analysis of the reverse factoring company.

- Trade acceptances notification: Using magnetic media, the reverse factoring company sends a list of trade acceptances as a payment proposal, indicating the beneficiary, amount, bank account and expiration date. Suppliers cannot access financing until they receive notification from the reverse factoring entity.

- Interest payment, by means of a discount, in the event of advance payment of the invoices by suppliers: The number of days for the computation of interest includes those from the value date of collection until the expiration date of the invoice.

- Interest payments: In the case of financing from the reverse factoring company: At the end of each settlement period. It is usually formalised through a credit agreement.

- Guarantee: Once the invoices have been made, the financial institution can guarantee their payment.

- Formalization: By specific contract. The funding, according to an agreement in accordance with the instrument used.

- Term: It is usually one year, at the end of which it can be renewed.

The task of the financial institution consists of:

- To receive from the company the invoices payable and communicate it to the suppliers.

- To sign the corresponding claims assignment contracts with suppliers who wish to advance the collection of their invoices.

- To send, at the expiration of each invoice, cheques or transfers to suppliers that have not advances the collection.

- Thus, the supplier can wait for the invoices to expire to collect or can choose to collect their invoices before the due date, signing a claims assignment contract with the reverse factoring entity.

Advantages of reverse factoring

Reverse factoring provides several advantages, such as:

For the company:

- Improves its payment system.

- Management tasks are eliminated and transferred to the financial institution.

- Improves its planning and its cash forecasts.

- Improves supplier management.

- Avoids the costs of issuing promissory notes and cheques or of handling bills of exchange.

For the supplier:

- Gains agility and speed in the management of its invoices.

- It has a quick and easy financing system.

- Gets a credit facility without increasing its bank risk.

- Once the invoice is confirmed, it can collect it in cash, under preferential financial conditions and eliminates the risk of non-payment.

- Savings in the cost of using negotiable instruments.

Reverse factoring costs

What is the cost of a reverse factoring?

- Commission for payment management: Percentage of the nominal amount of the invoices managed, subject to a minimum. It relates to the suppliers administration and payment service provided by the bank. The percentage may vary depending on whether there is or not a direct debit.

- Interest in case of financing to the reverse factoring company: The result of applying the agreed interest rate to the balances drawn down during the financing period.

- Interest in the event of payment in advance by the supplier: The result of applying the agreed interest rate to the nominal amount of the invoices whose collection is advanced.

- Collection process commission: Percentage of the nominal amount of the invoices whose collection is advanced, subject to a minimum.