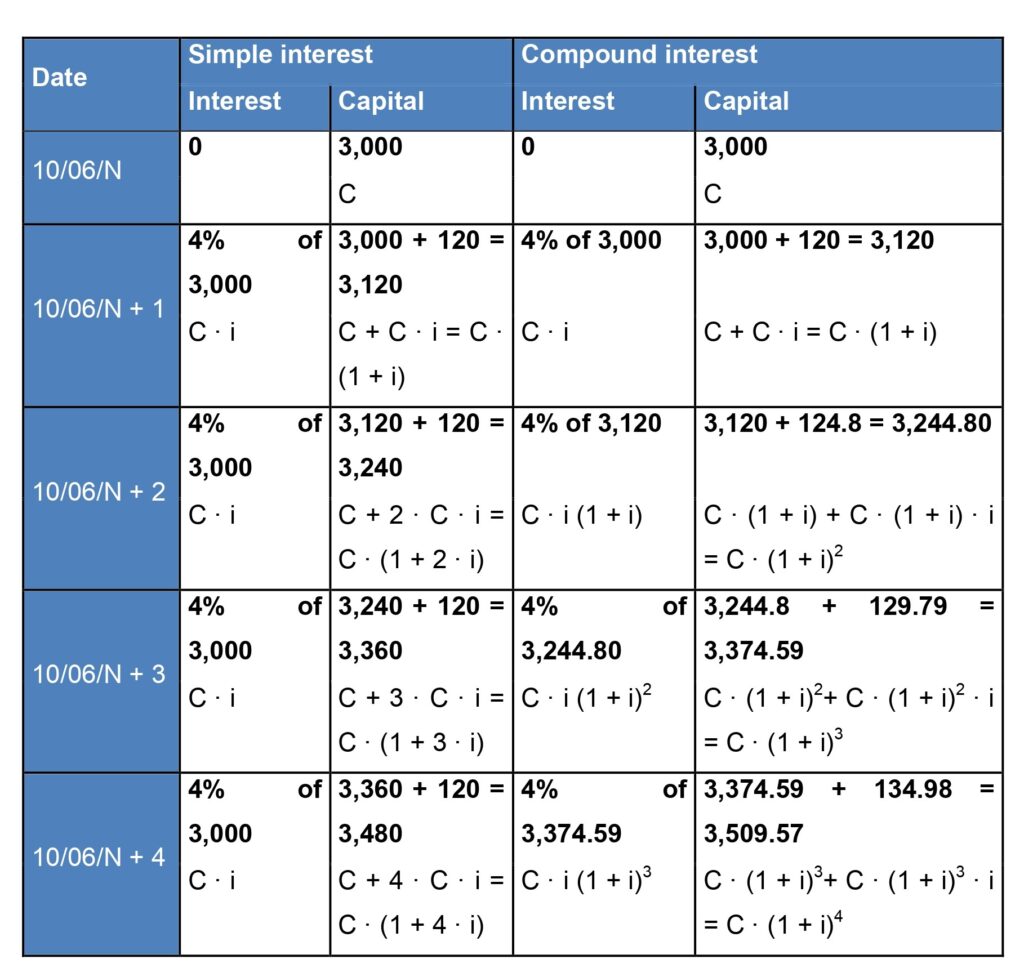

Depending on how interest is calculated, two capitalization laws are derived:

- Simple interest law: It is characterized by the fact that the interests are always the same for every term.

Example: If a person has 100 c.u. and assuming that the interest rate is 10% per year (interest that is not received until the full term ends), in a simple interest law each year (as long as this person has transferred the capital) this person is going to get 10 c.u., without taking into account that the accumulated money is growing. In this law, it can be understood that only the initial 100 c.u. produce interest.

Final capital = Initial capital x (1 + no. of terms x one-term interest rate)

- Compound interest law: In this law, as money generates interest, in addition to the initial capital, these interests generate new interest, so that the capital grows more quickly.

Example: A person takes 3,000 c.u. (C) on June 10 to a financial institution that offers an annual interest of 4% (0.04 expressed as a decimal).

Final capital = Initial capital x (1 + one-term interest rate) No. of terms

The following table shows the calculation of the money that person will get in 4 years according to the two laws. In this example, it can be seen how the effect of compound capitalization translates into interest 29.57 c.u. higher than that derived through simple compounding at the end of the period:

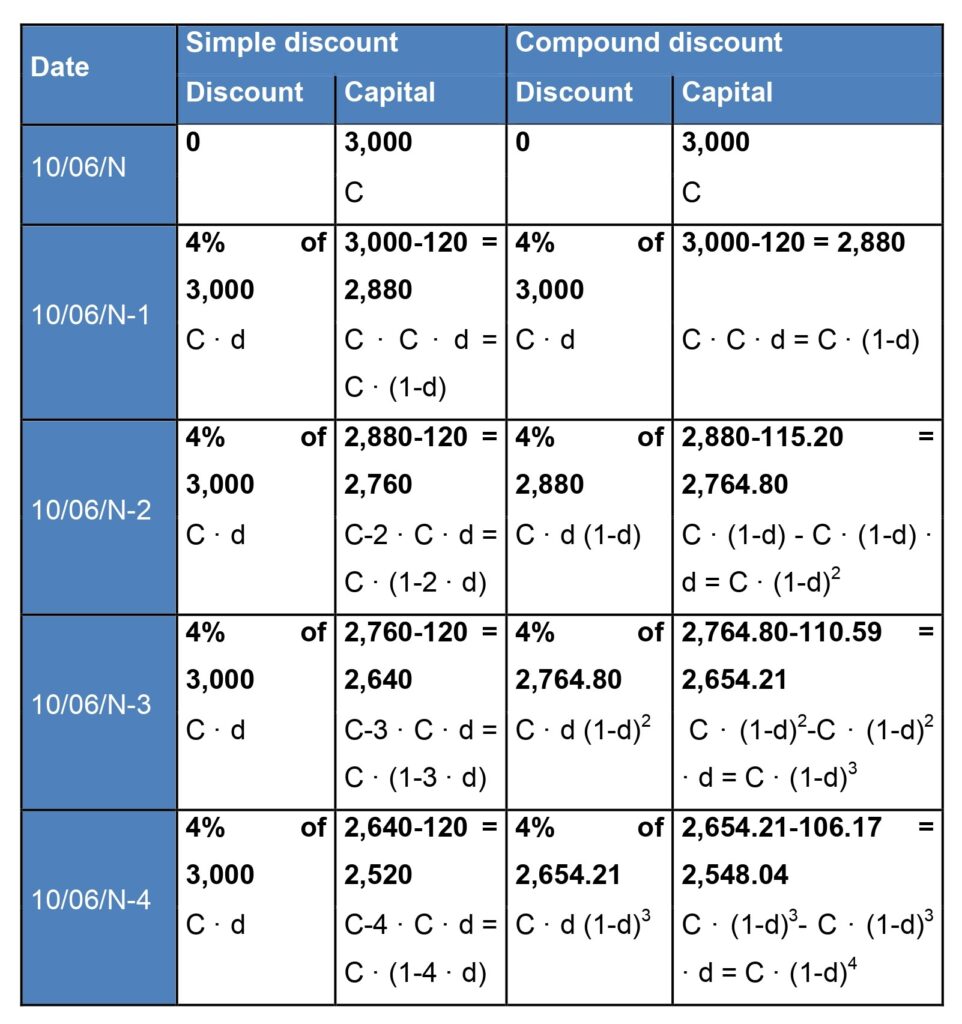

On the other hand, depending on how the discounts are calculated, two discount laws exist:

- (Commercial) simple discount law: It is characterized by the fact that the discount is always the same for every term. For example, if a person has 100 c.u. and assuming that the discount rate is 10%, in a simple discount law each year they will deduct 10 c.u. In this law, it can be understood that the discount is always calculated on the 100 c.u.

Initial capital = Final capital x (1 – No. of terms x one-term discount rate)

- Compound discount law: In this law, as the money is reduced, new discounts are generated, that is, the discount is calculated on the previous discounted capital.

Initial capital = Final capital x (1 – one-term discount rate) No. of terms

Example: A person has a bill corresponding to a capital of 3,000 c.u. to be paid on June 10 within 4 years. This person wants to cash it on June 10 of the current year and, to this end, they resort to a financial institution that offers them an annual discount of 4%.

Next, the table calculates the money that person will receive according to the two laws: