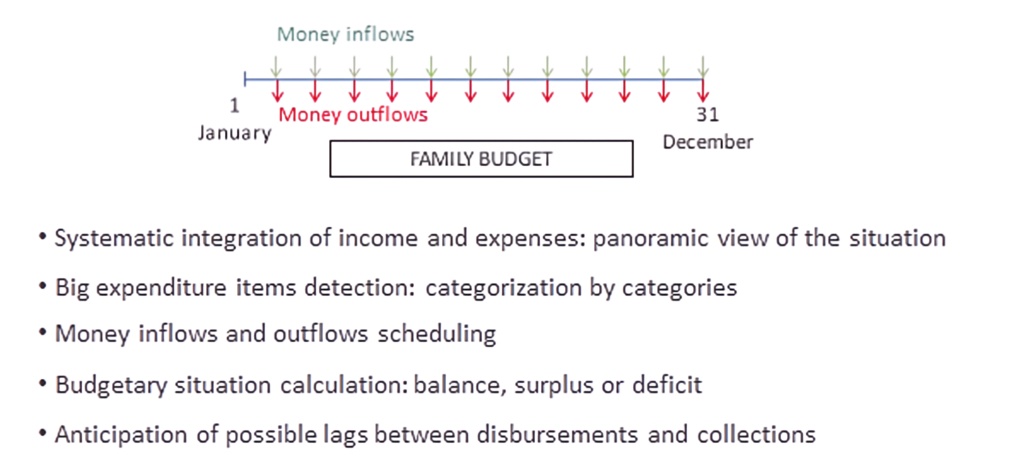

In order to manage their degree of financial freedom or financial autonomy, it is necessary that people measure their income and expenses, and compare them. This is called budgeting. Therefore, a family budget is a document that collects, in a coded, joint, systematic and orderly manner, the income and expenses of a family over a certain period. Normally, budgets are based on a calendar year. The following diagram includes what is indicated above together with a series of utilities when preparing a family budget:

On the other hand, in order to prepare correctly a family budget, it is necessary to know the different types of income a family can have:

- Income from employment: Wages.

- Income from capital: Interest on deposits, dividends, etc.

- Income from real estate investment: Rents received, etc.

- Income from economic activities: Business profit of self-employed persons, etc.

- Social benefits: Pensions, unemployment benefit, etc.

- Extraordinary income: Awards, inheritances, etc.

In the same way, it is important to take into consideration other aspects in relation to the income that a family receives:

- Time: The moment of collection may be different from the moment in which the right to be paid is generated.

- Taxation: Some income is subject to withholdings with regard to income tax and to social contributions.

- The possible additional tax burden must be borne in mind when filing the income tax return and the possible charge of other taxes.

Regarding the expenditure components, it is suitable to classify them because it will be easier to control them. Expenses are classified as follows:

- Current expenses: They are necessary for daily life. These are food, transport and clothing expenses, etc.

- Fixed costs: These are those to which a person agrees by contract (lease of the home, mortgage, loans, water, electricity, gas, etc.) or without a contract with third parties (school, nursery, etc.).

- Not fixed: They are adjustable (holiday’s enjoyment).

- Non-current expenses: They are irregular expenses. Some are unavoidable, such as medical expenses, but others can be reduced or even terminated if necessary. We can distinguish between investments, equipment and durable consumer goods and extraordinary expenses.

In order to follow a certain symmetry with respect to income, it is suitable to highlight other relevant aspects to be considered in relation to family expenses:

- Time: The moment of payment may be different from the moment in which the obligation of the expense is incurred.

- Taxation: Most spending transactions are subject to indirect taxes, so the total amount must be anticipated, as well as the possible ancillary costs.

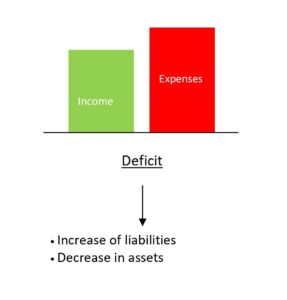

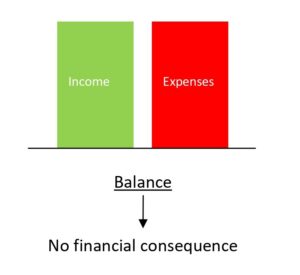

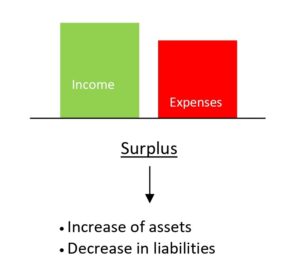

Once the possible income and expenses that a family may incur have been reviewed, attention must be paid to the budget balance. This is defined as the difference between inflows (income) and outflows (expenses). At the end of the period, the budget balance may present three situations:

- Balance: If the inflows are equal to the outflows, there will be a total balance, without any consequences for the future. It is important to note that even in this situation of global balance there may be temporary funding requirements.

- Surplus: If the inflows are higher than the outflows, there will be a surplus available with which to acquire new assets or to increase the balance of existing ones, or otherwise to reduce pending payment obligations.

- Deficit: If the inflows are lower than the outflows, an imbalance is generated and it has to be covered. It can be done in two ways:

- Use of the funds of the family’s net worth, which drives to a decrease in wealth.

- Income Expenses Deficit

- Increase of liabilities

- Decrease in assets